The post-election lull is a good time

for a financial check-up

Key takeaways:

- The end of election season is an ideal time for investors to reflect on the impact of the economy and financial markets on their long-term investment plans for the future.

- Objective financial guidance is indispensable for investors who want to achieve the goal of a secure and comfortable retirement.

November 6, 2024 – In addition to all the election noise over the last several months, investors have also faced stress over high inflation, shifting interest rates, the sustainability of the stock bull market, and the need to save and invest for retirement.

Now that the election campaigns are behind us, it’s an ideal time for investors to reflect on the current state of the economy and financial markets and how both may impact their long-term investment plans going forward.

Just before Election Day, we hosted a LinkedIn poll for financial professionals, asking what their clients were most concerned about with the election approaching. ‘Inflation and finances’ was by far the leading concern among more than half of the poll respondents.

Effective financial planning requires nuance, as there is no universal solution that fits all client circumstances. Objective guidance from a financial professional is indispensable for investors who want to achieve the goal of a secure and comfortable retirement.

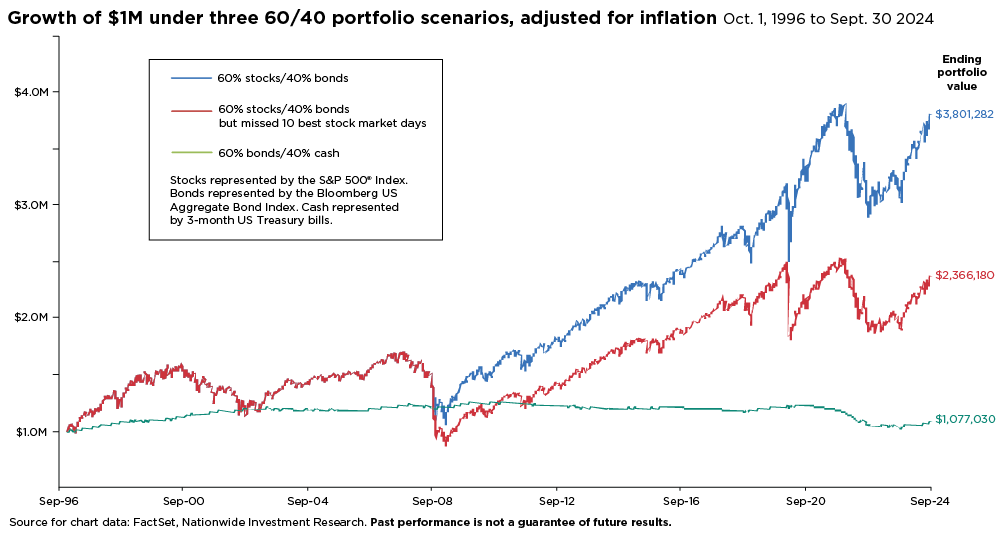

The accompanying chart illustrates the value of following a prudent investment strategy and the cost when emotions take over. It presents three hypothetical scenarios of portfolio performance for a traditional 60/40 investment allocation. Each scenario starts with $1 million on October 1, 1996, and maintains this allocation over 27 years until September 30, 2024. All three scenarios are adjusted for inflation.

The blue-line scenario represents a mix of 60% stocks (S&P 500® Index) and 40% bonds (Bloomberg U.S. Aggregate Bond Index). The red-line scenario shows the same allocation but assumes the investor misses the 10 best days for the S&P 500 over this 27-year period. Many of these best days have often occurred after significant drops in the stock market, when fearful investors are more likely to sell. The difference between the lines is stark; missing these 10 best stock market days over the last 27 years results in approximately 40% less wealth for the future.

The green-line scenario is the worst of the three. It illustrates the cost an anxious investor incurs by avoiding risk, holding 40% of their portfolio in cash (represented by 3-month Treasury bills) and the remainder in bonds (Bloomberg U.S. Aggregate Bond Index). Over a retirement span of 27 years or more, an overreliance on cash and bonds may fail to keep pace with inflation, increasing the risk that investors will struggle to meet expenses such as health care costs. Moreover, younger investors are likely to spend more years in retirement as life expectancy gradually increases, meaning more years of living expenses during retirement to plan for.

These examples demonstrate the different impacts that inflation, market timing, and portfolio construction can have on investors’ long-term financial goals. Maintaining a diversified and balanced portfolio over time gives investors the best chance to beat inflation, but it requires them to assume risk and stay disciplined through market volatility. Conversely, avoiding too much risk increases the likelihood that savings won’t keep pace with inflation. Acting on emotion can be detrimental to future financial health.

As the dust settles on the 2024 election, investors should take this time to meet with their financial professionals, conduct a portfolio check-up, and reassess their risk if needed. It’s also a good opportunity to define or refine their retirement investment plans and discuss other important financial matters, such as the impact of potential tax law changes on their portfolios.

Keep inflation in mind to help protect retirement savings

Author(s)

Mark Hackett, CFA, CMT

Chief of Investment Research, Nationwide Investment Management Group

Mark Hackett is the Chief of Investment Research for Nationwide’s Investment Management Group, bringing more than 20 years of experience in the asset management industry to the role.

Trending articles

In the coming years, more people will begin to think about the costs of health care in retirement and the possibility of needing long-term care (LTC) in the future, especially as the number of Americans reaching age 65 hits an all-time high this year.

Considerations for financial professionals on supporting retirees through economic uncertainty.

The Windfall Elimination Provision (WEP) is critical for financial professionals to understand.