Generation X seeks financial guidance to meet the realities of retirement

Key takeaways:

- Gen X investors face unique financial challenges, including supporting both older and younger family members while planning for retirement.

- Many Gen Xers are adjusting their financial plans, seeking professional guidance to manage inflation and market volatility.

- Flexibility and comprehensive planning are crucial for Gen X retirement security.

12/02/2024 — Generation X has been through a lot during their adult lives, and these experiences have helped shape their financial perspectives. They witnessed the stock market booms of the late 1990s and the 2010s, but also made it through the dot-com stock bust of the early 2000s, the global financial crisis and Great Recession of 2007-09, and the COVID-19 pandemic of 2020.

Now as Generation X gets closer to retirement, the realities of the financial challenges ahead are starting to feel more acute. Like other generations before them, many Gen Xers find themselves sandwiched between caring for older parents while still raising or providing for children. They’re also struggling to manage the emotional, physical, and financial costs of this support.

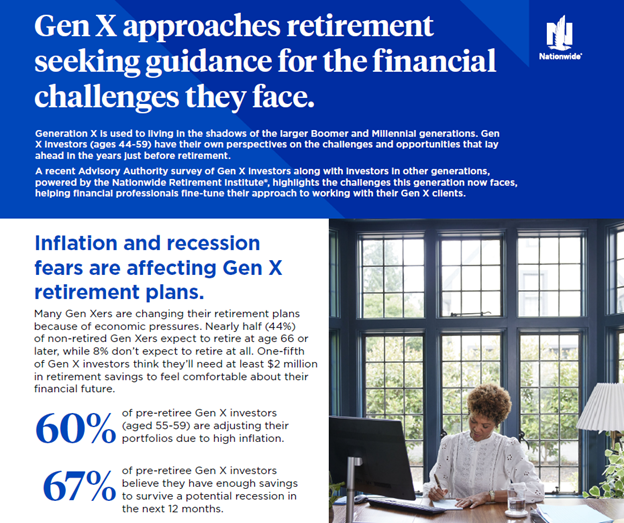

As part of the tenth annual Advisor Authority survey, powered by the Nationwide Retirement Institute®, we explored the specific challenges and concerns that Gen X investors are facing as they prepare for retirement. Many are adapting their financial plans to current economic conditions, but there’s plenty of opportunities for financial professionals to help their Gen X clients manage their specific financial concerns and feel better prepared for their financial future.

Gen Xers financial outlook for the next year: not good

Caring for older and younger family members complicates Gen X retirement plans

The idea of the “sandwich generation” is familiar to many of us in the financial industry. When people reach their late 40s or 50s, many find themselves “sandwiched” between dual caregiving responsibilities. On one side are older family members, commonly parents who require greater care and attention as they get older themselves. On the other is the younger generation—either minor children still living at home or adult children who may still be financially dependent on their parents.

The responsibilities of caring for older or younger family members, or both generations at the same time, can place tremendous strain on a financial plan. Many Gen Xers are feeling this strain today; more than half of Gen X investors are providing financial support to their older parents or younger children. Consequently, they’re running up credit card debt (24%) and cutting back non-essential spending (35%).

Also, importantly for Gen X investors as they approach retirement, these caregiving pressures have forced many to take actions that are potentially adverse to their personal retirement plans. Our survey found that one in five Gen Xers are unable to save for retirement, one in four have reduced or halted retirement savings, and one in six have made withdrawals from investment or retirement accounts to help ease the financial pressures they currently face.

Closing the gap with guidance from financial professionals

While some Gen Xers may be pessimistic about retirement today, their past experiences have helped them become more resilient and proactive in the face of financial challenges. Our survey found that 60% of pre-retiree Gen X investors have adjusted their portfolios in response to inflation. Another 67% believe they have enough savings to withstand a possible recession in the next 12 months.

Yet, many may find it challenging to balance the demands of providing financial support to family members while planning for their own financial futures. That’s why more Gen Xers are seeking out financial professionals for guidance. Our survey found an increase among Gen X investors paying for advisor services, up from 29% six months ago to 37% today.

In addition, Gen X clients of financial professionals report feeling more calm about market volatility and better able to avoid emotional decisions. These are both encouraging trends for the future financial security of this generation.

To help clients manage family-related expenses as they approach retirement, many financial professionals are leveraging tax deductions and credits or recommending long-term care insurance solutions that provide financial resources to care for aging family members.

Help Gen X clients build a comprehensive financial plan fit for their needs

As a financial professional, the guidance you offer to your Gen X clients can go a long way toward helping them build greater financial security for retirement.

As retirement becomes more of a reality for Generation X, flexibility becomes more important to their financial plans. You can help them continue to grow their retirement savings with investment strategies that manage the risk of market volatility. You can also design their financial plan to adapt to evolving economic conditions, helping to ensure they have the savings they need to provide income throughout a long retirement.

You can partner with Nationwide for resources and solutions that help you help your Gen X clients prepare for the financial road ahead. Turn to us for ideas for building a comprehensive financial plan, with strategies for generating retirement income, protecting wealth or managing retirement and long-term care costs.

Author

Craig Hawley

President, Nationwide Annuity

Craig Hawley is President of Nationwide Annuity, a top 10 seller of annuity products in the U.S., representing more than $110 billion in assets.

Trending articles

In the coming years, more people will begin to think about the costs of health care in retirement and the possibility of needing long-term care (LTC) in the future, especially as the number of Americans reaching age 65 hits an all-time high this year.

Considerations for financial professionals on supporting retirees through economic uncertainty.

The Windfall Elimination Provision (WEP) is critical for financial professionals to understand.