Retirement income spending sets a good balance.

Many Americans, whether retired or still working, see their retirement savings and income as a means for enjoying retirement. Nearly half of U.S. adults (48%) intend to spend all of their retirement savings and income to get the most out of their life in retirement.

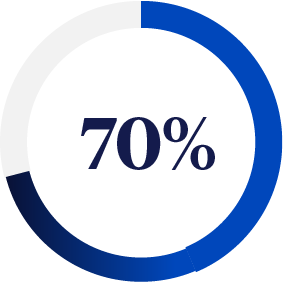

Percentage of income retirees spend on essential expenses* (or for those who are not retirees, expect to spend) on average.

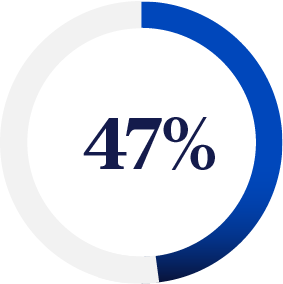

One-half of American adults (50%) don’t know what percentage of their income their Social Security benefits will replace or replaced in retirement.

Percentage of non-retired adults who expect their living expenses to stay the same in retirement.

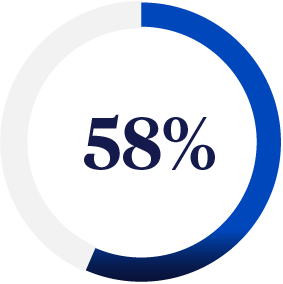

The average percentage of pre-retirement income that non-retired adults expect to need in retirement.

Clients place high importance on maximizing Social Security.

Here’s the opportunity for financial professionals to help clients by addressing concerns about Social Security and their retirement finances. Many current clients want to discuss ways to reduce the impacts of inflation and taxes on their retirement income, as well as financial strategies to help maximize their Social Security benefits.

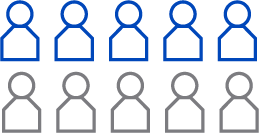

4 in 5

of current U.S. adults with a paid financial professionals or prospective clients who want to talk to a financial professional about Social Security would switch professionals if their financial professional could not show them how to maximize their Social Security benefits.

Help your clients build a plan for Social Security and retirement income.

With insights and resources from the Nationwide Retirement Institute®, you can answer client questions around when to file for Social Security benefits and how to help maximize their retirement income.

![]()

Learn more about our tools to help optimize Social Security benefits.