Lessen the impact of the partisan divide with financial guidance

10/23/2024 — Key takeaways:

- Rising uncertainty and anxiety could create more volatility in the market and contribute to emotional investment decisions.

- Past election cycles have shown that these volatile spells are always temporary and don’t last long.

- Investors should focus on the real drivers of financial market performance—the economy and corporate earnings, not election results.

Around this time last year, many market analysts harbored a rather pessimistic outlook for market returns in 2024. However, both stocks and bonds have defied these gloomy predictions and performed admirably through the first nine months of the year. The S&P 500® Index has surged over 22% year-to-date, while the Bloomberg U.S. Aggregate Bond Index has gained nearly 4.5% year-to-date and an impressive 11.5% over the past 12 months, as of September 30. Remarkably, the S&P 500 is also on pace to deliver its strongest performance leading into an election year since 1932, underscoring just how misplaced those initial forecasts were.

What’s encouraging about this performance is that investors haven’t been as reactive as might have been expected, given all the reasons for increased volatility—not only the uncertainty about the imminent presidential election but also rising geopolitical tensions and lingering recession concerns.

As a case in point, the CBOE Volatility Index (VIX) gauge, which measures expected stock market volatility, has averaged around 15 this year—its lowest average since 2017. Between 2020 and 2023, the VIX average was around 23, so this year’s lack of volatility represents a significant departure from the norm.

Even though many investors may see links between election outcomes and the performance of the market or their investments, the fact is that stocks have historically performed well no matter which party controls the White House or Congress. But as we quickly approach Election Day 2024 and the partisan divide among voters remains as wide as ever, the likelihood of investor anxiety grows. Higher anxiety could create more volatility in the market and contribute to emotional investment decisions.

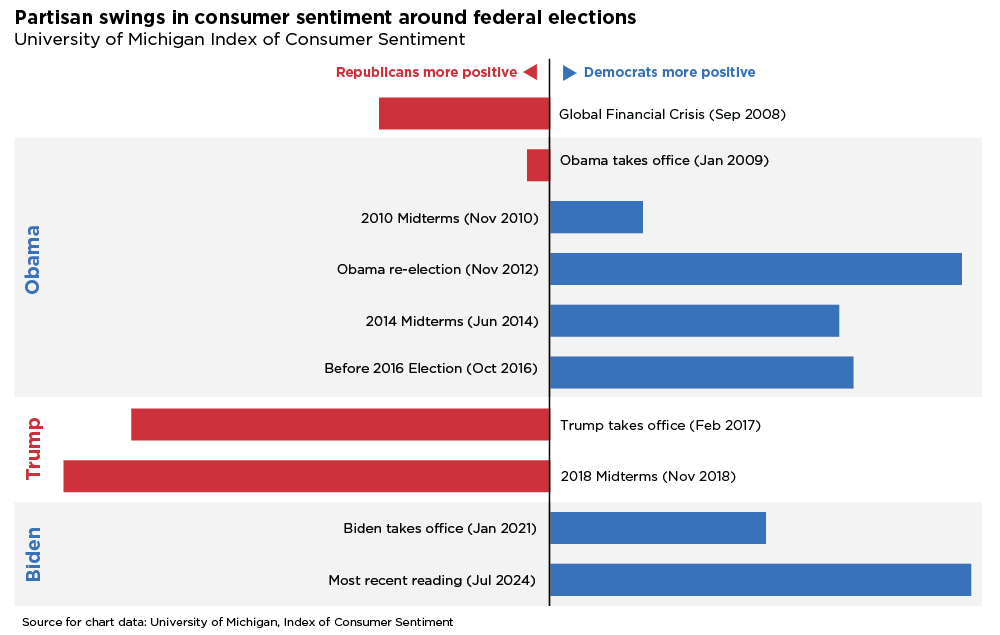

To see the influence of political partisanship in financial terms, consider the accompanying chart (updated this year for our “Investing in a Highly Politicized Climate” paper). The chart depicts the gap in consumer sentiment between Republicans and Democrats as measured by the University of Michigan Consumer Sentiment Survey. After 2009, in the post-Global Financial Crisis era when Barack Obama took office, the partisan swings in consumer sentiment grew pronounced.

During the Obama administration, Democrats were broadly satisfied with the state of the economy, while Republicans were largely dissatisfied. These sentiments shifted almost immediately after Donald Trump’s election victory in 2016; optimism surged among Republicans, while Democrats became widely pessimistic.

A similar shift occurred after Joe Biden won the 2020 presidential election—Democrats were as optimistic about the economy as Republicans were despondent. In both cases, nothing else had essentially changed except control of the Executive Branch. In the most recent reading of this indicator (July 2024), consumer sentiment remained strong among Democrats but has dropped to multi-year lows among Republicans.

When looking at this data, I always go back to the idea that things are never as bad as people may think when they’re on the losing side, and likewise never as good as they think when they’re winning. This is an important message to reinforce with investors as we enter the final stages of this election season.

Forecasting the effects of election outcomes on the financial markets is just a guessing game. With so much uncertainty and investor trepidation in the air, the potential for volatility shouldn’t be ignored. However, past election cycles have shown that these volatile spells are always temporary and don’t last long.

While it may be hard for investors to tune out the election noise in the next few weeks, the best guidance they can get right now is to focus instead on the real drivers of financial market performance—the economy and corporate earnings, not election results. A recent Advisor Authority survey found that a majority of investors—Democrats, Republicans, and Independents—said that working with a financial professional during an election year helps them feel more secure. This guidance may be just what clients need to lessen the impact of the political divide.

Author(s)

Mark Hackett, CFA, CMT

Chief Market Strategist, Nationwide Investment Management Group

Mark Hackett is the Chief Market Strategist for Nationwide’s Investment Management Group, bringing more than 20 years of experience in the asset management industry to the role.

Trending articles

In the coming years, more people will begin to think about the costs of health care in retirement and the possibility of needing long-term care (LTC) in the future, especially as the number of Americans reaching age 65 hits an all-time high this year.

Considerations for financial professionals on supporting retirees through economic uncertainty.

This guide explores strategies for securing long-term care for children with special needs through special needs trusts, ABLE accounts, and government benefits.