Help clients overcome barriers to planning for health care costs in retirement

09/19/2024 — Key takeaways:

- High medical costs and debt burdens are affecting how many people save for retirement, according to our latest health care costs in retirement survey.

- Among a majority of adults, there’s widespread doubt about Medicare’s future and misunderstanding about how Medicare works.

- Financial professionals can help address the uncertainties around retirement health care costs by simplifying financial planning and decision making.

Concerns about the future of Medicare contribute to the uncertainty many Americans feel about managing health care costs in retirement. The high cost of living today is already squeezing many households, which can make planning for future health care needs including medical expenses and costs for extended care seem like a lower priority.

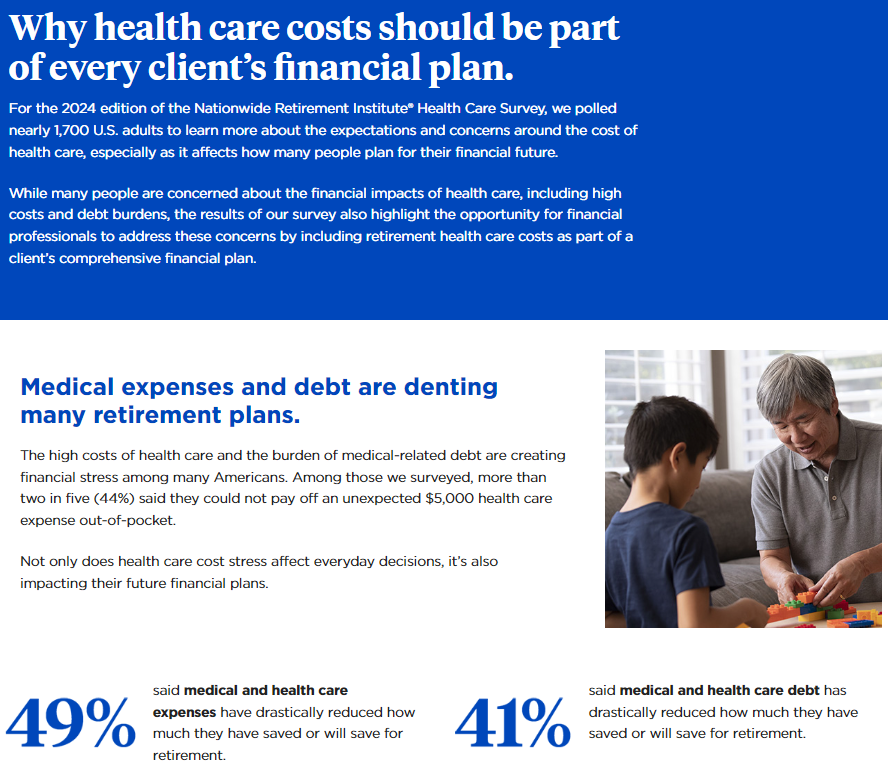

The latest edition of the Nationwide Retirement Institute® Health Care Cost in Retirement survey polled nearly 1,700 U.S. adults to learn more about the expectations and concerns around the cost of health care and its impact on their financial future.

As financial professionals and solutions providers, we need to address the uncertainties and ease the fears around retirement health care costs. The best way we can approach these topics is to simplify the financial planning and decision-making processes.

Health care spending today is affecting saving for tomorrow

For many people, the financial impacts of health care in the present day—from rising costs, to increased debt burdens—are affecting their ability to save for tomorrow. Almost half of adults we surveyed (49%) said they have drastically reduced how much they have saved or will be able to save for retirement because of current medical and health care expenses.

Insurance policies and savings products like Health Savings Accounts (HSAs) can help with medical expenses and managing out-of-pocket costs. But a surprise or emergency health care expense has the potential to be financially devastating. Many people have to borrow or use credit cards to cover unplanned health care costs, which can have an adverse effect on people’s ability to save for their financial future. Around two in five adults (41%) said medical debt has drastically reduced how much they have saved or will be able to save for retirement.

With many people struggling to balance their household budgets and pay their bills on time, planning for health care needs in the future often takes a back seat. In our survey, 70% of adults said they’re not sure or can’t estimate how much their expected retirement health care costs will be.

Medicare misgivings and misunderstandings

The general consensus is a majority of Americans will rely on Medicare to help cover a significant share of their health care expenses in retirement. Despite the importance of the program to so many people, there is widespread doubt about Medicare’s future and a lot of misunderstandings about how the different parts of Medicare actually work.

Let’s start with the misgivings. More than three in five adults (63%) worry that Medicare won’t be available in the future when they will need it. But these feelings of doubt shouldn’t deter people from planning for future health care costs. Financial professionals should acknowledge them but keep clients focused on estimating the cost of their future health care needs, then designing a financial plan to help cover these expected costs.

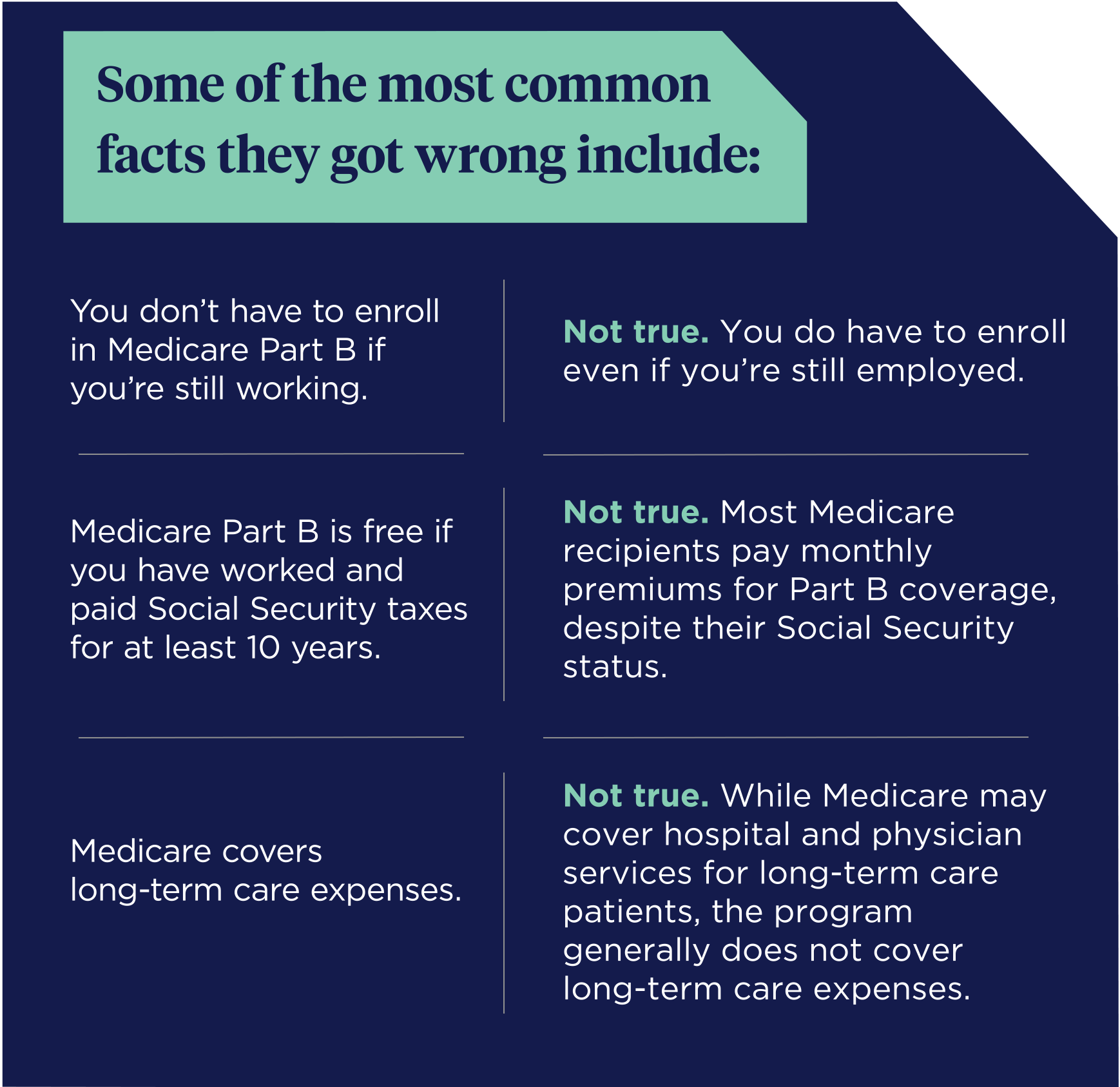

Next, the level of misunderstanding about Medicare shouldn’t be surprising—two in three (67%) said they wished they understood Medicare coverage better. Many people are unfamiliar with the basics, which offers financial professionals a good place to start their health care planning discussions with clients.

For example, we quizzed survey respondents on some of the basics of Medicare. In a true-or-false question format, many people either answered the questions incorrectly or weren’t sure.

While there is strong desire among clients to learn more about health care cost planning, and specifically about the ins and outs of Medicare, most clients of financial professionals aren’t getting this as part of financial planning. Nearly three in five of those surveyed who pay to work with a financial professional (57%) report that their financial professional has not provided advice on how and when to file for Medicare benefits.

Your guidance is valuable when planning for health care costs in retirement

As a financial professional, you have an opportunity to enhance the value you bring to your client relationships by helping to fill this knowledge gap and work with clients to develop plans to cover a major expense they’ll face in retirement.

Over four in five adults (83%) agreed that managing health care costs should be part of personal financial planning in retirement.

How can you help? A good place to start is by debunking some misunderstandings clients may have about health care in retirement and Medicare. The most popular Medicare topics that people want to learn about from a financial professional when discussing retirement planning include:

- Overall costs of Medicare coverage (41%)

- What the different parts of Medicare (A, B, C, D and Medigap) cover (37%)

- Out-of-pocket costs depending on the Medicare plan they have (34%)

As a financial professional, you can proactively address the importance of planning for medical expenses in retirement, including decisions around Medicare enrollment and benefits. A well-informed plan is key to helping your clients secure their financial futures.

How you can help your clients when planning for health care in retirement

Nationwide can help with resources and solutions that help you clarify and simplify all the decisions your clients make around planning for retirement health care costs. Consultative support from our Nationwide Retirement Institute® specialists can help you solve complex financial planning scenarios and build personalized plans for clients for covering retirement health care costs.

Plus, tools such as the Nationwide’s Health Care Cost Estimate can help you present a more accurate picture of a client's expected retirement health care needs and expenses. You can also use our newest white paper, “Medicare Explained: Answers to Client Questions”, to prepare for client conversations and help them navigate the complexities of their Medicare decisions.

Author

Kristi Martin Rodriguez

SVP, Nationwide Retirement Institute

Kristi Martin Rodriguez currently serves as Senior Vice President of Thought Leadership for Nationwide Financial, leading the teams responsible for advocating for and educating members, partners and industry leaders on issues impacting their ability to have a secure financial future.

Trending articles

In the coming years, more people will begin to think about the costs of health care in retirement and the possibility of needing long-term care (LTC) in the future, especially as the number of Americans reaching age 65 hits an all-time high this year.

Considerations for financial professionals on supporting retirees through economic uncertainty.

The Windfall Elimination Provision (WEP) is critical for financial professionals to understand.