Loading...

Funding a trust with life insurance

Key takeaways

- Consider life insurance as a funding vehicle for an existing credit shelter trust arrangement or other irrevocable trusts that were established and funded in the past.

- Life insurance can help minimize income taxes paid by the trust during a surviving spouse’s lifetime and at death, as well as minimize the potential impact of the 3.8% Medicare surtax.

- Another funding option is a nonqualified deferred annuity; life insurance may offer an advantage for remainder beneficiaries with an income tax-free death benefit1 and potentially better value if the surviving spouse dies in a short time period after purchasing the life insurance, because the remainder beneficiaries would receive the full death benefit with fewer premiums paid.

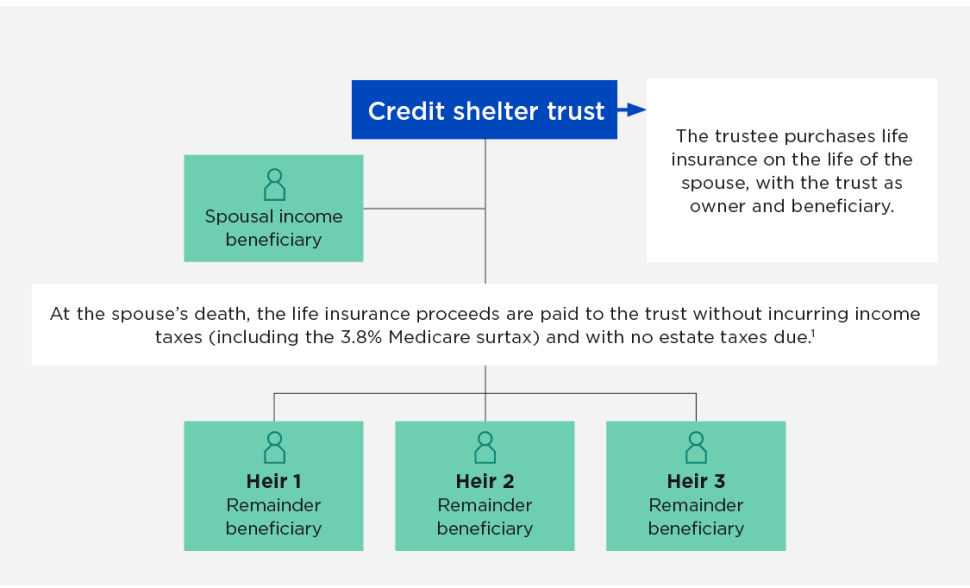

Trusts are an essential part of legacy planning, and funding a trust with life insurance is a popular funding method. A common scenario is one in which a spouse passes away and leaves assets to the surviving spouse in the form of a credit shelter trust (also known as a bypass trust, A/B trust or “B” trust). In this scenario, the surviving spouse does not need the income generated by these trust assets. But if the trustee leaves the income in the trust, the trust is on the hook for taxes that could be as high as 40.8%. (The top trust tax bracket is 37% + a 3.8% Medicare surtax, if applicable.) The trustee wants to avoid the trust paying tax but does not want to make a distribution of the income out of the trust. So what can be done to avoid the trust paying tax on the income?

An example

In 2017, Reggie Milton passed away and a credit shelter trust was funded with assets worth $5,490,000, which was equal to his available applicable exclusion amount for federal estate tax purposes. Reggie’s surviving spouse, Roberta, is the income beneficiary of the trust, and their children, Roger, Renee and Rosa, are remainder beneficiaries in equal shares. Roberta does not need the income generated by the trust assets; thus, the trust is subject to significant income taxes as well as the Medicare surtax.

Solution

The trustee uses the credit shelter trust assets to purchase a life insurance policy on Roberta’s life. The trust is named as owner and beneficiary of the life insurance policy, and Roberta is the insured. Upon Roberta’s death, the proceeds of the life insurance policy are paid to the credit shelter trust free of income and estate tax (including the 3.8% Medicare surtax).1 Thereafter, the insurance proceeds can be distributed to Roger, Renee and Rosa — also income and estate tax free.1 By using life insurance as a funding vehicle in the trust, the trustee will be able to take advantage of several of the general benefits and features of life insurance. In addition, the trust can provide distributions during the surviving spouse’s life.2

- The surviving spouse may have a right to receive the income and often has a right to receive principal (under certain limited criteria) from the trust.

- The trust may allow the children as beneficiaries of the trust to receive distributions for any reason.2

- If the policy is structured properly, the cash value can be accessed (as withdrawals or loans) income tax free (including the 3.8% Medicare surtax) to make distributions to the surviving spouse and/or the children.2

The information provided is based on current laws, which are subject to change at any time. Parties considering this strategy should consult with their tax advisor regarding earnings and distribution taxes.

Cautions

- If distributions of the policy’s cash value will need to be made during the surviving spouse’s life, the policy should not be a modified endowment contract (MEC). If the policy is considered a MEC, withdrawals of the policy’s cash value may be subject to income tax.

- When trust assets are sold to purchase the life insurance, any gain may be taxable income to the trust or the trust beneficiaries (if the taxable income is distributed to the trust beneficiaries) in the year the trust assets are sold.

Book time with our Retirement Institute Planning team or contact the team at iplndesk@nationwide.com.

[1] The surviving spouse must not possess any “incidents of ownership” in the policy under IRC Sec. 2042; for example, if the surviving spouse is a trustee of a credit shelter trust. Please consult with an attorney or legal advisor. The death benefit is not subject to federal income tax unless a taxable transfer for value under IRC Sec. 101(a)(2) is applicable.

[2] If the life insurance policy is a modified endowment contract (MEC), withdrawals of policy cash value may be subject to current income tax, including the 3.8% Medicare surtax.

Related topics & resources

Older couple walking through forest together

Nationwide CareMatters®

This single-life coverage is for clients who are primarily looking for long-term care coverage and want to be able to recover their costs if they never need care.

Nationwide CareMatters is a service mark of Nationwide Mutual Insurance Company.